I guess i didn't heed her advice, with all this messy posts with no clear direction and spelling/vocab mistakes. I would therefore like to make it clear that my agenda is purely monetary in terms of the capital invested, that's all. Nothing else. Like what the bank robber said ," Give me the money and no one gets hurt" kind of Caveman like mentality.

Disclaimer: I am not an investment advisor. Heck, i am not even working in the financial industry. Below are my interpretation and i am grateful if you will let me know if anything i say is wrong and i will correct it in a reasonable time. I am not an expert and don't wish to be assumed to be one. I make losses frequently.

The Lucky Accredited Investors

$300 million 5.75% Perpetual Capital Securities (ISIN: SG6OE1000007)

In 15 January 2014, these were issued to them in denominations of $250,000.

First reset is on 23 January 2017 and subsequent resets occur every three years thereafter.

I couldn't find the step up rates.

The Accredited investors who bought this had theirs redeemed on 23 January 2017. Lucky you!

$175 million 4.8% Perpetual Capital Securities (ISIN: SG6SC0000003)

In 21 July 2014, these were issued to them in denominations of $250,000.

First reset is on 29 July 2016 and subsequent resets occur every two years thereafter.

I couldn't find the step up rates.

The Accredited investors who bought this had theirs redeemed on 29 July 2017. Lucky you!

The Unlucky Non-Accredited Investors

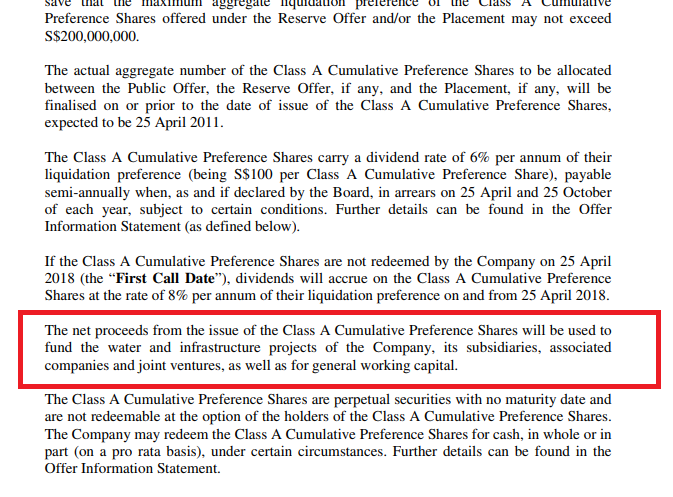

$400 million 6% Cumulative, Non-Convertible, Non-Voting, Perpetual Class A Preference Shares (N2H)

In April 2011, these were issued to them in denominations of $1000 but a minimum of $10,000.

First reset 25 April 2018 and step up to 8% pa thereafter. See here.

Not redeemed on 25 April 2018.

$500 million 6% Perpetual Capital Securities (BTWZ)

In May 2016, these were issued to them in denominations of $1000.

First reset 27 May 2020 and step up to the initial spread at 4.20 per cent. per annum plus the step-up margin of 2.00 per cent. per annum. See here.

Not redeemed and even had its coupon stopped, even after being publicly announced and ex-coupon

Observations

Firstly, who are accredited investors. Read here.

In short, they are:

i) Individuals with a personal net asset in excess of $2 million;

ii) Individuals with an income of not less than $300,000 in the past 12 months;

iii) Corporations with net assets exceeding $10 million in value, in their most recent balance sheet;

iv) Trustees of trusts that the MAS approves; or

v) Persons that the MAS approves

Based on the dates of issue and redemption, it does give me an impression that retail, non- sophisticated really got the short end of the stick.

$500 million 6% Perpetual Capital Securities issued in May 2016.

I guess part of the retail investors money was used to pay back the Accredited Investors as their was redeemed on July 2016 and January 2017.

The unlucky unsophisticated retail investors in terms of the BTWZ got it worst with its coupon withheld.

Now, for .....................

Question 11

Why did the the board, in 2016 and 2017, when they redeemed the perpetual securities from the Accredited Investors , not have the foresight to not redeem them since their interest rates were so low at 5.75% and 4.8% respectively compared with 6% for the retail investor ones?

Wouldn't it be beneficial to hold a cheaper " debt" longer?

Can you give some colour on the step-up rates given to the Accredited Investors issue?

Can you shed some light on why there was a need to raise such funds from the accredited investors since Hyflux seemed to have excess cash to be able to conduct sharebuybacks in 2014 and 2015?

I don't know about you, but i'm left with a very bad taste in my mouth.

Further reading

1) Considerations about Hyflux2) The fate of Hyflux

3)Will Hyflux recover? The billion dollar question

4) Hyflux-Treatmeat of perpetual share holders- Ezion

5) Hyflux - loans and borrowings - Pacific Radiance

6)A happy ending for retail perpertual securities holders - Tiger Air and Hyflux

7) The Very Curious Case of Sharebuybacks- Hyflux

8)What did the founder/Chairwoman/CEO do to help hyflux throughout the years

9) Moving forwards at the Townhall meetings with Hyflux - Part 1

10) Moving forward at the Townhall meeting with Hyflux - Part 2