TODAY published an article on 3 December 2008 on the sale of Singapore Food Industries to Singapore Airport Terminal Services ( SATS). . The Editor used the market capitalisation of Singapore Food to state whether the sale price was at a discount or premium.So is market capitalisation a good measure of whether an acquisition is cheap or expensive?

TODAY published an article on 3 December 2008 on the sale of Singapore Food Industries to Singapore Airport Terminal Services ( SATS). . The Editor used the market capitalisation of Singapore Food to state whether the sale price was at a discount or premium.So is market capitalisation a good measure of whether an acquisition is cheap or expensive?Let's give an example, if 2 slaves each cost $4. ( just for simplicity sake lah...we hate slavery...don't be soooo uptight!). If one slave has a debt of $1 but another has a debt of $3. If a master was to buy a slave and he has to pay back the debt owed by the slave, which is actually a more expensive buy? Of cos the slave who has a debt of $3 is the more expensive buy. On the same token, if one slave has $1 dollar in his pocket and the other has $2 in the pocket. When you buy a slave, you get his dollar in the pocket. So in this instance, the slave who has $2 in the pocket is a cheaper buy as you get to pocket the $2. So let's use this concept to measure whether the buy price of Singapore Food is cheap or not, shall we?It is actually a well used concept with a jargonic name called Enterprice Value.

Enterprise Value ( EV) = Market Cap + Debt - Cash

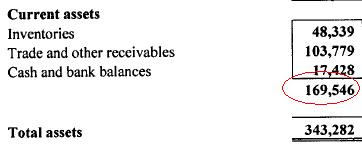

Debt = $74,968,000 (ABOVE)

Cash = $17,428,000 (ABOVE)

Cash = $17,428,000 (ABOVE)  From above, it is stated that 69.68% represents 359,731,154 shares. This means the number of shares outstanding for Singapore Food is 516,261,702 (100%)

From above, it is stated that 69.68% represents 359,731,154 shares. This means the number of shares outstanding for Singapore Food is 516,261,702 (100%)Calculating...........

Enterprise value = 516,261,702 X 0.89( Using the price given in the above TODAY article) + 74,968,000 - 17,428,000 = 517,012,915

Therefore, the theoretical cost of the acquisition if we based on market-determined price of 89 cents listed on the Singapore Stock exchange in TODAY's article should be $517,012,915. If we divide it by the total number of shares = 517,012,915 / 516,261,702 = $1.0015 per share.

The cost of the acquisition to SATs if they are able to acquire all the shares in the market place based on last done market- determined price of 89 cents on the Singapore Stock Exchange in the TODAY paper above is therefore theoretically ( academically) actually $1.0015 per share. Mainstream media states 93 cents as the price paid per share.

But what is the true true true true true true true cost that it paid? Since SATs paid 93 cents. Based on the below calculation,

516,261,702 X 0.93+ 74,968,000 - 17,428,000 = 537663382.86

537663382.86/ 516,261,702 (shares)=$1.04 per share!!

(This article has been heavily edited after contributions from readers. SGDividends SUCKS!! )

Important: The objective of the articles in this blog is to set you thinking about the company before you invest your hard-earned money. Do not invest solely based on this article. Unlike House or Instituitional Analysts who have to maintain relations with corporations due to investment banking relations, generating commissions,e.t.c, SGDividends say things as it is, factually. Unlike Analyst who have to be "uptight" and "cheem", we make it simplified and cheapskate. -The Vigilante Investor, SGDividends Team

Does this makes sense or just the other way round?

ReplyDeleteEnterprise Value (EV) = Market Cap + Debt - Cash

So more debt, less cash means enterprise value increased?I think the term 'Enterprise Value' is misleading.

The equation is ofcos correct but its does not imply the 'value' of the firm. It merely represents the true cost of the acquisition.

SATS paid 93cts cash but after the net debt assumed the actual cost will be the $1.01 calculated.

Hence its incorrect to say that there is a discount of 7%. It should be the actual cost will be 8.6% higher.

Hi CC,

ReplyDeleteYou know something. We thought about it and we think you make sense.

Enterprise value should be intepreted as the true cost of the acquisition and not as the value of the firm as for example:

Company A has $100 cash

Company B has $400 cash.

Ceteris Paribus.

It does not make sense that Company B is valued less than Company A since it has more cash. (Enterprise Value (EV) = Market Cap + Debt - Cash)

Therefore, taken in context, the cost of acquisition to SATs is actually $1.0015 instead of 93 cents.

Which means the cost to SATs is actually 0.0715/0.93 = 7.7% more than 93 cents.And they actually "paid" more.

Agreed. Will update the above.

Thanks CC =)

jus wondering......should EV be computed using the offer price 0.93 (actual acquisistion price) by SATS instead of 0.89 (mkt last done price) ??? if we are talking abt acquisition cost here ?

ReplyDeleteHi Anonymous,

ReplyDeleteEnterprise Value (EV) = Market Cap + Debt - Cash

Are you refering to Market Cap?

Market Cap is using market price X number of oustanding share. This is considered what the general market values SingFood seen in the Singapore Exchange (SGX). This is based purely on academic theory used by companies before they takeover a company to find the true cost of take over.So maybe SATS did this theoretical calculation first before. Maybe.

We know what you mean actually. Since SATS pay 0.93 per share and SATs still have to pay debt and after minusing off the cash, the real real cost to SATs is actually

516,261,702 X 0.93( Using the price given in the above TODAY article) + 74,968,000 - 17,428,000 = 537663382.86

537663382.86 / 516,261,702=1.04

This is the real real cost : $1.04.And the Economic value ( Cost of acquisition in the market place) = $1.0015.

This comment has been removed by the author.

ReplyDeleteQuote: "This article has been heavily edited after contributions from readers. SGDividends SUCKS!! "

ReplyDeleteDon't be that harsh lah... it's just different ways of looking at/interpreting the figures.

You are super funny la. :)

ReplyDeleteIt's always enjoyable reading your posts.

Btw, I think SATS did make a good move in a strategic viewpoint. They have always been wanting to branch out for a few years already.

Paying a premium for a company which have tentacles extended outside is usually reasonable for acquisitions. Just only how much.

But as according to your post above, it seems that maybe they got a fair deal?

There are so many ways of valuating the business but what is more important is what SATS is going to do with the new acquisition in the long run.

hi Dancerene,

ReplyDeleteIts ok. We are used to self critism and we have low self esteem. Maybe cos we are small in built =)

Hi PassiveLifeIncome,

Thanks!Yeah, it just makes perfect sense for SATS to buy SingFood.

Anyway Singfood has been providing food services for Commercial ships. Now it will include Commercial planes!

Like to throw in the tale of BenQ buying Siemens mobile phone division for the grand price of -250 million euro (yes, the negative is not a typo) in 2005. The strategic goal of this deal is that BenQ wants to compete with the big boys(eg. Nokia,Motorola) in the global market.

ReplyDeleteSiemens gave the division to BenQ along with that cash gift in exchange for the promise that BenQ keeps the factory and jobs in Germany. The total debts and liabilities nearly bankrupted BenQ 1 year later...and Siemens mobile phones became collectibles and a footnote in history.

Of course, providing packaged food and mobile phones are very different business with different cost structure. But still amusing to think about that deal in terms of enterprise value and price per share.

Good article and thanks for highlighting this real real cost...in this era of media bombarding us with easily digestible bottom-lines and ratios.

I (~~) SGDIVIDENDS

\/