Disclaimer: I am not an investment advisor. Heck, i am not even working in the financial industry. Below are my interpretation and i am grateful if you will let me know if anything i say is wrong and i will correct it in a reasonable time. I am not an expert and don't wish to be assumed to be one. I make losses frequently.

Another anonymous Telegram member shared the article " Total Compliance in Financial Reporting, But is it misleading?"

In summary, i think this article can be distilled into 3 points:

- An illusion of recurring, steady profits is shown as Hyflux is allowed to recognise financial receivables/intangible assets as profits over the 20 to 30 year concession period. This has the effect of "smoothening" the profits. However, this had no link to cashflow.

- Since the cash payments of Preference and Perpetuals (PnPs), which are actually financial liabilities, can be deferred indefinitely, PnPs are recognised as equity under FRS32 . This allowed "interest payments" to be removed from the profit and loss statement and shown as dividends, giving an illusion of higher profits

- An illusion of low debt is also shown as Hyflux is able to classify PnPs under equity instead of under liabilities, hence enlarging the equity base and reducing the liability base. The Edge gave any example in 2014. showing the net gearing of 51% is shown but it should "actually" be 326%.

Within one year from issuing the guidelines by MAS , in 2016, the perpetual securities are issued to mom and pop investors who can gorge at it through the ATMs.

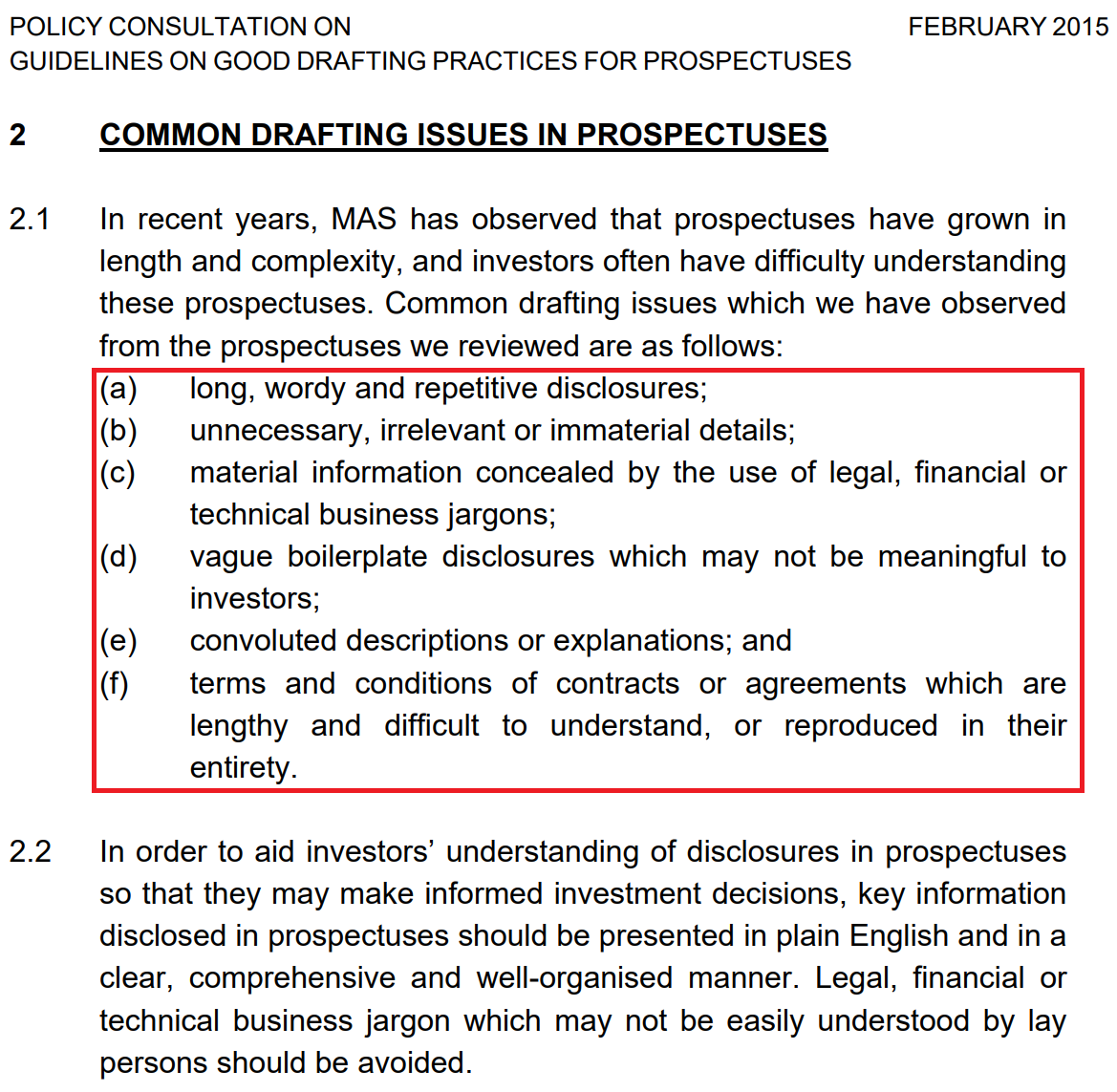

Let's compare the MAS Guidelines on Good Drafting Practices to the 197 page long Hyflux Offer Information Statement for the $500 million Perpetual Securities issued in 2016.

Were the guidelines followed?

I don't think the Hyflux Offer Information Statement in 2016 provided any sort of easily readable disclosure of the 3 " illusions" stated above which would facilitate investors' understanding of the true state of Hyflux.

This is called financial engineering whose only purpose , in my opinion, is to paint a rosier picture of a company.

Perfect Precision Timing By Olivia Lum and her Board of Directors

March 2016 - Tuaspring power plant went online

May 2016 - $500 Perpetual Securities offered for sale to retail mom and pops, retirees through ATMs.

August 2016 - Second quarter results ( ending 30 June 2016) released showing a plunge of 84% in profits.

Olivia Lum blamed the weak power market for the woes of Tuaspring.

It must be remembered that the power plant of Tuaspring went officially online on March 2016 and 2016 is the year when the USEP hit the all time low.

Within 2 months from the official opening of the Tuaspring power plant, in May 2016, Olivia Lum completed selling the $500 million perpetual securities.

This could have been the most opportune time to do so, before the second quarter, ending 30 June 2016, financial statements is out.

As seen above, Hyflux was profitable in calendar years 2013,2014 and 2015 and this rosy picture is painted to whet the appetite of the retail perpetual security holders, hook, line and sinker.

There was a short span of time between March and August 2016 for the perpetual selling to be done and sell she did, like hot cakes when it was upsized from the original $300 million to $500 million.

In August 2016, the 2nd quarter results showed a 84% plunge in profitability as shown below.

However, the perpetual securities had already been successfully offloaded to the retail market before the disastrous 2nd quarter 2016 results is out. CHEERS!

|

| 2nd quarter results 2016 |

It is true that the extremely astute investors who have been very proactive in following the company's announcements could have sold their holdings after the 2nd quarter results were out. However, this is not the point. These astute investors would have sold it to fellow retail investors again. There was no way these securities could be returned to the company. These toxic, " lemon" securities would still be floating about in the retail investor market, ensnaring other retail investors.

Back to the forum post question:

"HOW MUCH DID HYFLUX BOARD KNOW WHEN THEY OKAYED RETAIL BONDS?"

It still seems like a nightmare to me when some investors still had the mood to clap for her during the second townhall, still oblivious to what is really happening.

For PnP and MTN holders who wants to vote NO but are unable to attend the voting on 5th April 2019. You can fill up this form to proxy others. This has to be done by 31 March since 2 April is the deadline to give the forms to Boardroom, a Corporate Secretarial Company and some leadtime is necessary for the volunteers.

VOTE NO!

Further reading

1) Considerations about Hyflux2) The fate of Hyflux

3)Will Hyflux recover? The billion dollar question

4) Hyflux-Treatmeat of perpetual share holders- Ezion

5) Hyflux - loans and borrowings - Pacific Radiance

6)A happy ending for retail perpertual securities holders - Tiger Air and Hyflux

7) The Very Curious Case of Sharebuybacks- Hyflux

8)What did the founder/Chairwoman/CEO do to help hyflux throughout the years

9) Moving forwards at the Townhall meetings with Hyflux - Part 1

10) Moving forward at the Townhall meeting with Hyflux - Part 2

11)The Lucky Accredited Investors of Hyflux's Perpetual Securities - Part 3

12) The Peculiar Case of HyfluxShop - Question 12

13)Uncovering the Real Motivations Behind the HyfluxShop

14) High Level Staff Movement Indication of Red Flags -Hyflux

15)An industry comparison of Hyflux compared with its peers - Question 15

16)What other Water Companies did that Hyflux didn't - Question 16

17)Why a debt to equity option for retail investors is not right

18) Consolidated Questions For Hyflux Townhall Meeting on 19 and 20 July 2018 - Hyflux

19)Consolidated Questions For Hyflux Townhall Meeting on 19 and 20 July 2018 - Hyflux- continued

20)Informal Steering Committee for the Reorganisation Process - Hyflux

21) What happened to other Debt Restructuring Exercises - Ausgroup

22)What happened to other Debt Restructuring Exercises - Nam Cheong

23) My layman views of the so-called " White Knights of Hyflux"

24) The Unsecured Working Group (UWG) are against the retail investors - Hyflux

25)Where to find money to pay back retail investors?

26)What happened at Hyflux's Second Townhall Meeting

27) Another bomb to the retail investors of Hyflux

28)The Underrated Importance of Regulatory Risk - Hyflux

29)The Overlooked Importance of Another Regulatory Risk - Hyflux

30)Why did so many Singaporeans invest in Hyflux - The positive image illusion

31)On Why The Rich Get Richer And Poor Gets Poorer - The Hyflux Proposal is Out!

32)The " not spoken much" dirty little thing about the Restructuring Proposal - the $33 million - Hyflux

33) The Failure of the much touted Public-Private-Partnership Model in Singapore - Hyflux

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.