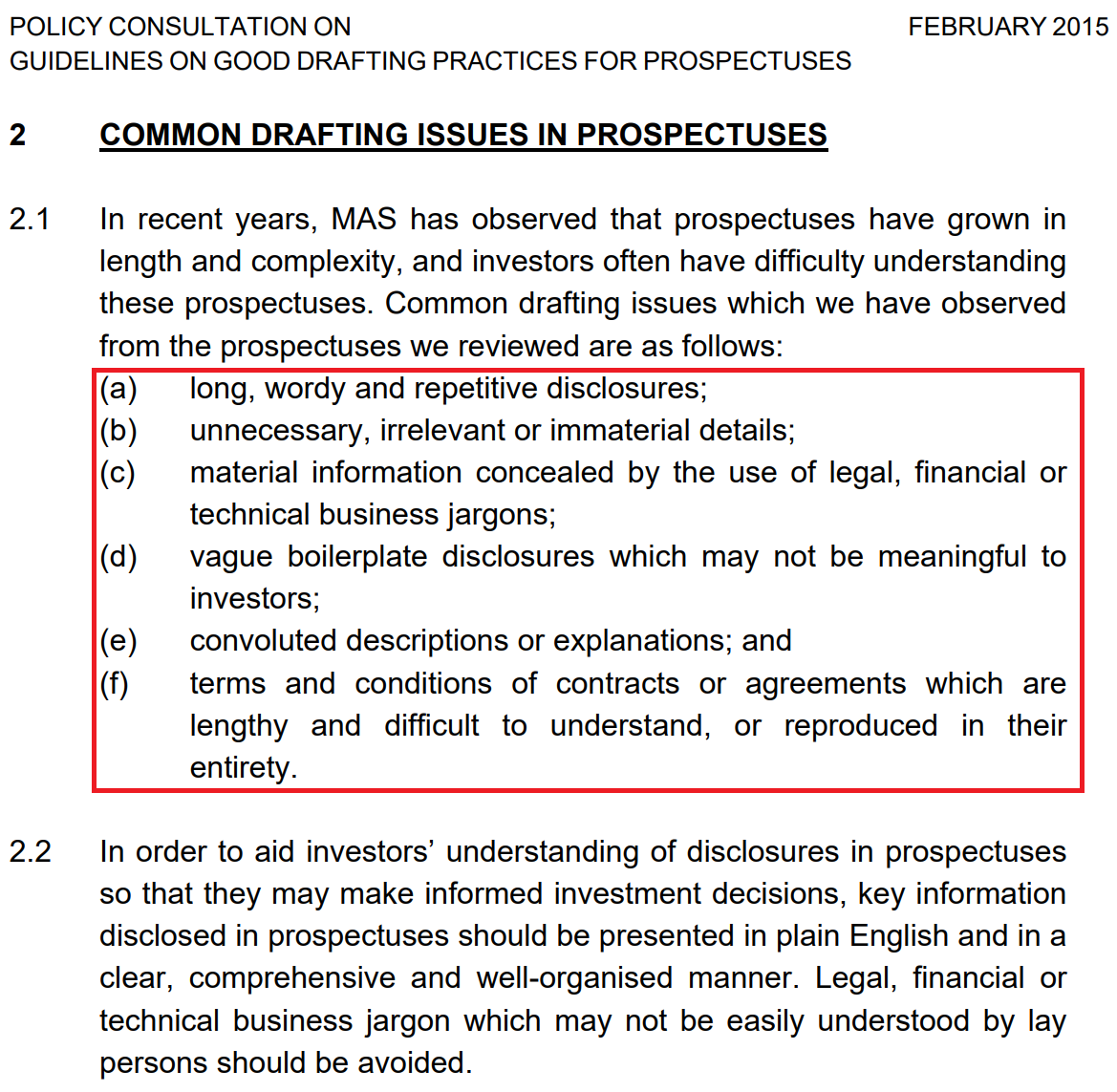

Disclaimer: I am not an investment advisor. Heck, i am not even working in the financial industry. Below are my interpretation and i am grateful if you will let me know if anything i say is wrong and i will correct it in a reasonable time. I am not an expert and don't wish to be assumed to be one. I make losses frequently.

An anonymous Telegram member shared this article " Who Audits the ' Big Four' Auditing Firms" posted by Channelnewasia on 29 May 2018. I find this question very apt for the current Hyflux. episode

- On 16 February 2019, Hyflux uploaded a court affidavit. In it, information about key projects were highlighted.

It came as a surprise that three of the key projects was last audited on Dec 2016. Of particular note was the "elephant in the room", the project at the very heart of this saga, Tuaspring. It must be noted that Hyflux's Annual Report for 2017 ( calendar year ending 2017) has been released and the accounts signed off by their auditor, KPMG on 22 March 2018.

In the notes to the financial statements, KPMG also stated on page 142 of the annual report 2017.

Take note that Hyflux Group only had $1 billion recorded as net asset value on on its balance sheet and a loss of $115 million in 2017 as stated in Annual Report 2017. This means that any of the 6 projects listed above are significant.

If substantial subsidiaries like Tuaspring, Tuasone and Tlemcen which together comprises of more than 60% of the total projects has not been audited for the year ending 2017, how sure can KPMG be about the true financial state of Hyflux when they signed off on 22 March 2018 for the Annual Report 2017?

Can the Annual report 2017 be relied upon?

I am unable to find any disclosure in the Annual Report 2017 that Tuaspring, Tuasone and Tlemcen was last audited in 2016 only. Is this a material disclosure which would have raised some alarms?

- The Public Utilities Board (PUB) mentioned that defaults at Tuaspring have started as early as 2017. It was also mentioned in the court affidavit on 15 November 2018 that PUB has step-in rights to take over Tuaspring.

|

| 15 November 2018 Court Affidavits |

Since warnings have been issued to Tuaspring in 2017, why wasn't this disclosed in any way in the annual report 2017?

I was also unable to find in the offer information statement (OIS) of the $500 million perpetual securities or the annual report of 2017 that PUB had the right to take Tuaspring and at what cost?

My Thoughts

The audited financial statements for 2017 was signed off by KPMG on 22 March 2018 and barely 2 months later, on 23 May 2018 a court protection was called for.

22 March 2018 - Annual report 2017 signed off by KPMG

23 May 2018 - Court protection

Going - Concern ( Taken from Annual report 2017)

|

| Responsibilities of Auditors |

For Hyflux, it seems 2 months is all it takes to be considered a going concern.

There was already a material uncertainty existing in 2017 when PUB warned Hyflux about the defaults , hence casting doubts about Hyflux as a going concern. Why wasn't it disclosed?

Did the annual report 2017 paint a true and fair view of the financial position and performance of the company?

For PnP and MTN holders who wants to vote NO but are unable to attend the voting on 5th April 2019. You can fill up this form to proxy others. This has to be done by 31 March since 2 April is the deadline to give the forms to Boardroom, a Corporate Secretarial Company and some leadtime is necessary for the volunteers.

VOTE NO!

Further reading

1) Considerations about Hyflux2) The fate of Hyflux

3)Will Hyflux recover? The billion dollar question

4) Hyflux-Treatmeat of perpetual share holders- Ezion

5) Hyflux - loans and borrowings - Pacific Radiance

6)A happy ending for retail perpertual securities holders - Tiger Air and Hyflux

7) The Very Curious Case of Sharebuybacks- Hyflux

8)What did the founder/Chairwoman/CEO do to help hyflux throughout the years

9) Moving forwards at the Townhall meetings with Hyflux - Part 1

10) Moving forward at the Townhall meeting with Hyflux - Part 2

11)The Lucky Accredited Investors of Hyflux's Perpetual Securities - Part 3

12) The Peculiar Case of HyfluxShop - Question 12

13)Uncovering the Real Motivations Behind the HyfluxShop

14) High Level Staff Movement Indication of Red Flags -Hyflux

15)An industry comparison of Hyflux compared with its peers - Question 15

16)What other Water Companies did that Hyflux didn't - Question 16

17)Why a debt to equity option for retail investors is not right

18) Consolidated Questions For Hyflux Townhall Meeting on 19 and 20 July 2018 - Hyflux

19)Consolidated Questions For Hyflux Townhall Meeting on 19 and 20 July 2018 - Hyflux- continued

20)Informal Steering Committee for the Reorganisation Process - Hyflux

21) What happened to other Debt Restructuring Exercises - Ausgroup

22)What happened to other Debt Restructuring Exercises - Nam Cheong

23) My layman views of the so-called " White Knights of Hyflux"

24) The Unsecured Working Group (UWG) are against the retail investors - Hyflux

25)Where to find money to pay back retail investors?

26)What happened at Hyflux's Second Townhall Meeting

27) Another bomb to the retail investors of Hyflux

28)The Underrated Importance of Regulatory Risk - Hyflux

29)The Overlooked Importance of Another Regulatory Risk - Hyflux

30)Why did so many Singaporeans invest in Hyflux - The positive image illusion

31)On Why The Rich Get Richer And Poor Gets Poorer - The Hyflux Proposal is Out!

32)The " not spoken much" dirty little thing about the Restructuring Proposal - the $33 million - Hyflux

33) The Failure of the much touted Public-Private-Partnership Model in Singapore - Hyflux