Disclaimer: I am not an investment advisor. Heck, i am not even working in the financial industry. Below are my interpretation and i am grateful if you will let me know if anything i say is wrong and i will correct it in a reasonable time. I am not an expert and don't wish to be assumed to be one. I make losses frequently.

The " white knight" may not rescue the princess after all.

On 18 March 2019, Hyflux issued an announcement with the following paragraph:

"Hyflux Ltd or Tuaspring Pte Ltd ceasing or threatening “to cease for any reason to carry on its business in the usual and ordinary course” is a “Prescribed Occurrence” within the meaning of the Restructuring Agreement."

This is in response to PUB's recent announcement about the operational and/or financial defaults of Tuaspring which started since 2017. This "Prescribed Occurrence" allows Salim to walk away.

So it seems not only retail investors are not fed material information before, even an institutional investor , who has the utmost complete advantage of resources and the benefit of the comprehensive court affidavits are not aware of such material information when doing their due diligence.

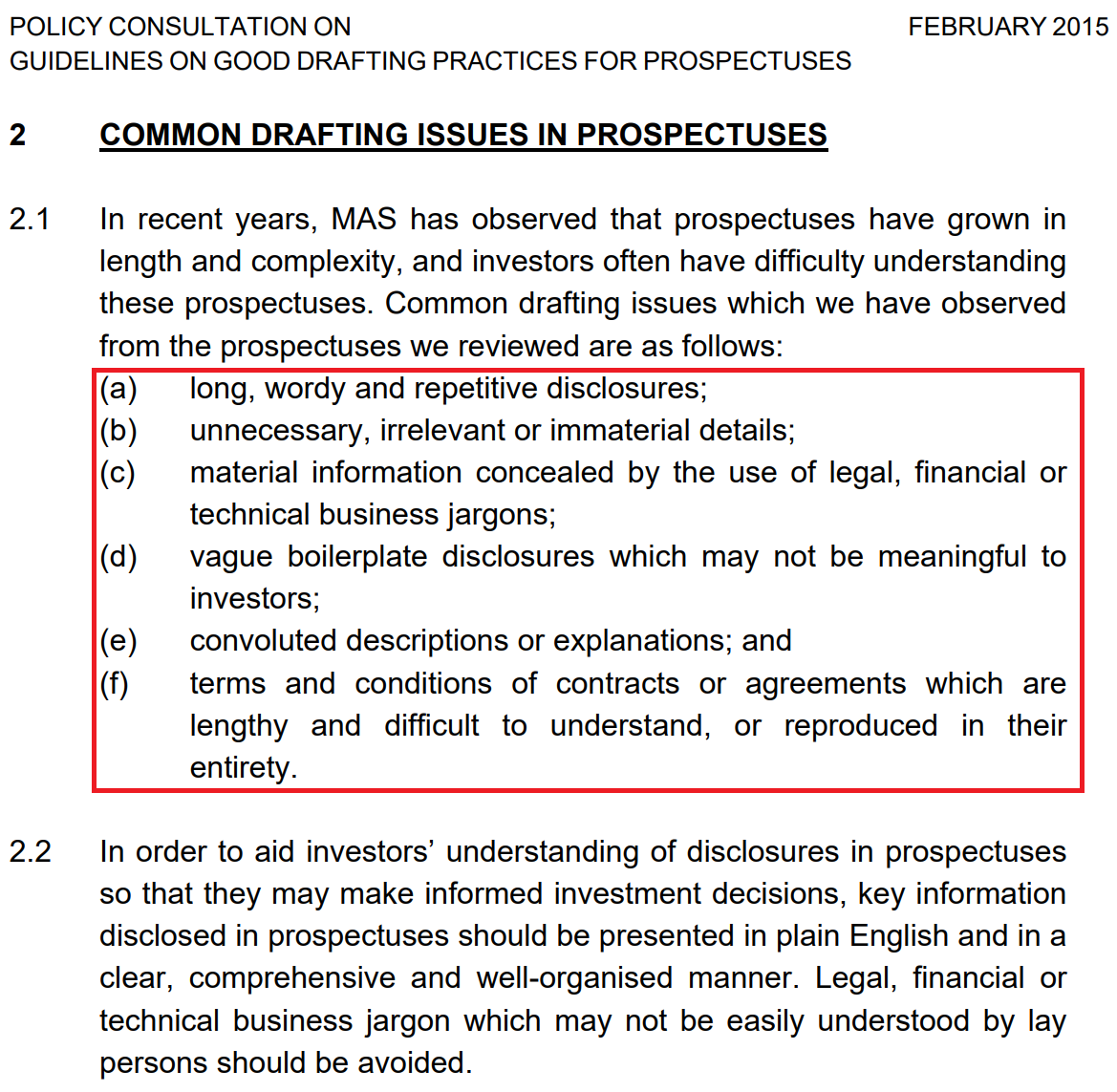

But the above is not the point of this article. The point of this article is to discuss about Singapore Exchange's (SGX) listing rules.

In particular, Practice Note 10.1 Shareholder Approval for Major Transactions.

SGX listing rule

In short, a listed company has to seek shareholder approval when they enter into a new business outside their existing core business.

The listing rule went as far as to state that even if the company is not entering into a new business and yet makes a transaction which will change the existing risk profile of the company, shareholder approval should still be sought.

Hyflux Annual report 2009

Hyflux Annual report 2010

My Thoughts

Before Tuaspring, Hyflux was in the water business.

By taking on Tuaspring in 2010, building a power plant is the first for Hyflux.

I hope you can see how misleading the power plant narrative was pitched " ...to provide an uninterruptible supply of good quality, clean energy to the desalination plant...".

I also hope you can see how stunned investors were when it was recently revealed during court protection that 10% of revenue is from water and 90% is from electricity.

Tuaspring is not a desalination plant with a power plant as an ancillary, instead its a power plant with a desalination plant as an ancillary

Hyflux has actually entered into a new business ( electricity generation) that has drastically changed the risk profile of the company.

To further elaborate my point, the power plant was completely unnecessary for the desalination plant to exist because Tuaspring operated without the power plant from 2013 to 2016.

Tuaspring was taking electricity from the grid instead.

In fact, the funny thing was, (USEP ) electricity prices was high in 2013 - 2015 and Hyflux was still doing well without the integrated power plant, despite needing to pay high prices to buy electricity from other generation companies.

It was only when the power plant at Tuaspring went online in 2016 that losses started to mount.

Imagine how profitable Hyflux would have been in 2016 ,2017 and 2018 since (USEP) electricity prices was at an all time low!

Let us read the reply from SGX when this issue was brought up to their attention.

SGX first reply

I think SGX is equally misled as i was.

"...objective of power plant ...was meant to supply electricity to the desalination plant."

"...Excess power will then be sold to the power grid."

As i wrote before, a 90% revenue from electricity does not reflect the objective of the power plant and also does not account for how an "excess' commodity can translate into such a high revenue.

Naturally, i replied and stated my points about revenue again, just in case, this point was overlooked.

SGX second reply

**I am not sure if you noticed, this second reply wasn't addressed to MAS anymore.

I am not sure if SGX got my point right when it stated:

"...There was no change in the primary infrastructure business of the Company."

I was refering to the time when Tuaspring was conceived in 2010 and Hyflux certainly didn't pitch itself as an infrastructure business then which seems like a catch-all phrase.

See my printscreen for the Annual report 2009 above again.

The paragraph in the red box takes the cake.

SGX defined "transaction" as acquisition.

Since Tuaspring is built by Hyflux and is not acquired by Hyflux, this rule does not apply to Hyflux.

I am not sure if SGX is being overly legalistic here.

Doesn't building a power plant require acquisition of power plant turbines (reportedly SGD$800 million and from here also ) and other power plant components?

Irregardless of whether they built or acquire, haven't the risk profile of Hyflux changed drastically which necessitated the point of requiring shareholder;s approval?

Naturally, i thought it was ridiculous and if i am not a reasonable person, i would be thinking that SGX is defending Hyflux. Thankfully, i think i am a reasonable person and i think SGX is just being misled.

My reply was a lengthy one, mentioning capital expenditure of power plant components in relation to the total project cost and market capitalisation of Hyflux during that time to illustrate how significant this Tuaspring " acquisition/built" was.

SGX third reply

** MAS not addressed too.

When SGX writes like this ".....we cannot determine or intervene in the commercial decisions of listed companies...", i wonder how they act as a front line regulator.

And this phrase " commercial decisions" seems the vogue this days. Everyone seems to be using it.

" Shareholders........have been given the opportunity at AGMs to raise questions and clarify any issues that they may have...."

My interpretation is " your opportunity is gone now" and there is nothing we can do about it.

Do you feel like there are adequate safeguards in place in Singapore to represent the retail shareholders? I certainly don't.

For PnP and MTN holders who wants to vote NO but are unable to attend the voting on 5th April 2019. You can fill up this form to proxy others. This has to be done by 31 March since 2 April is the deadline to give the forms to Boardroom, a Corporate Secretarial Company and some leadtime is necessary for the volunteers.

VOTE NO!

Further reading

1) Considerations about Hyflux2) The fate of Hyflux

3)Will Hyflux recover? The billion dollar question

4) Hyflux-Treatmeat of perpetual share holders- Ezion

5) Hyflux - loans and borrowings - Pacific Radiance

6)A happy ending for retail perpertual securities holders - Tiger Air and Hyflux

7) The Very Curious Case of Sharebuybacks- Hyflux

8)What did the founder/Chairwoman/CEO do to help hyflux throughout the years

9) Moving forwards at the Townhall meetings with Hyflux - Part 1

10) Moving forward at the Townhall meeting with Hyflux - Part 2

11)The Lucky Accredited Investors of Hyflux's Perpetual Securities - Part 3

12) The Peculiar Case of HyfluxShop - Question 12

13)Uncovering the Real Motivations Behind the HyfluxShop

14) High Level Staff Movement Indication of Red Flags -Hyflux

15)An industry comparison of Hyflux compared with its peers - Question 15

16)What other Water Companies did that Hyflux didn't - Question 16

17)Why a debt to equity option for retail investors is not right

18) Consolidated Questions For Hyflux Townhall Meeting on 19 and 20 July 2018 - Hyflux

19)Consolidated Questions For Hyflux Townhall Meeting on 19 and 20 July 2018 - Hyflux- continued

20)Informal Steering Committee for the Reorganisation Process - Hyflux

21) What happened to other Debt Restructuring Exercises - Ausgroup

22)What happened to other Debt Restructuring Exercises - Nam Cheong

23) My layman views of the so-called " White Knights of Hyflux"

24) The Unsecured Working Group (UWG) are against the retail investors - Hyflux

25)Where to find money to pay back retail investors?

26)What happened at Hyflux's Second Townhall Meeting

27) Another bomb to the retail investors of Hyflux

28)The Underrated Importance of Regulatory Risk - Hyflux

29)The Overlooked Importance of Another Regulatory Risk - Hyflux

30)Why did so many Singaporeans invest in Hyflux - The positive image illusion

31)On Why The Rich Get Richer And Poor Gets Poorer - The Hyflux Proposal is Out!

32)The " not spoken much" dirty little thing about the Restructuring Proposal - the $33 million - Hyflux

33) The Failure of the much touted Public-Private-Partnership Model in Singapore - Hyflux